Mega Gas Stations, $130B bet on Jeff Bezos, The anti-Zara retailer, Big Pharma in Space and Stubhub is run by a scalper

38th Edition

Greetings folks and a warm welcome to the 38th Edition of Friday Finance,

Uganda’s Chief of Defence Forces, General Muhoozi Kainerugaba, went on X last week to inform Jay-Z that he is, in fact, the poorer man, on the grounds that Jay-Z owns no Ankole cattle and the general owns thousands. Let’s run his numbers. A good Ankole cow fetches about $1,000; even a record auction bull tops out near $600K. Jay-Z is worth about $2.5B, so matching him on livestock takes roughly 2.5 million ordinary cows, or 4,000 champion bulls. “Thousands of cattle” gets the general to maybe a few million dollars, which is to say he undershot his own brag by about x1,000. He also threatened to take the dispute to the United Nations, which does not, to my knowledge, have a livestock-valuation subcommittee. Let's get right to it.

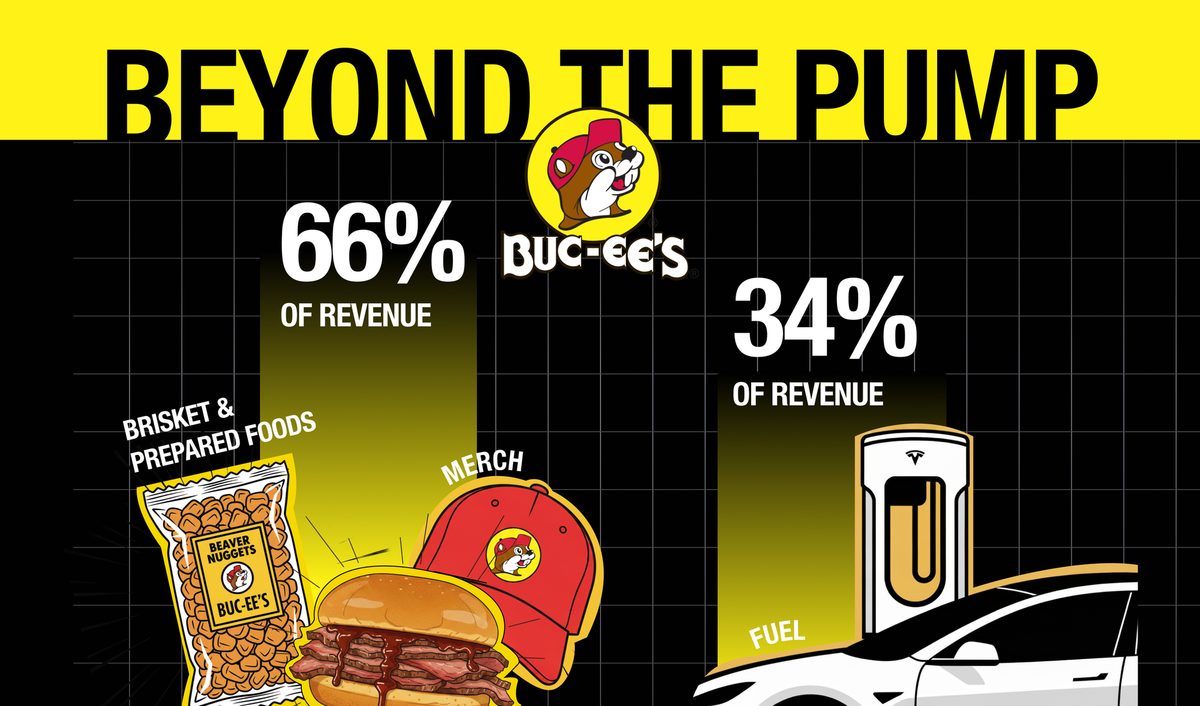

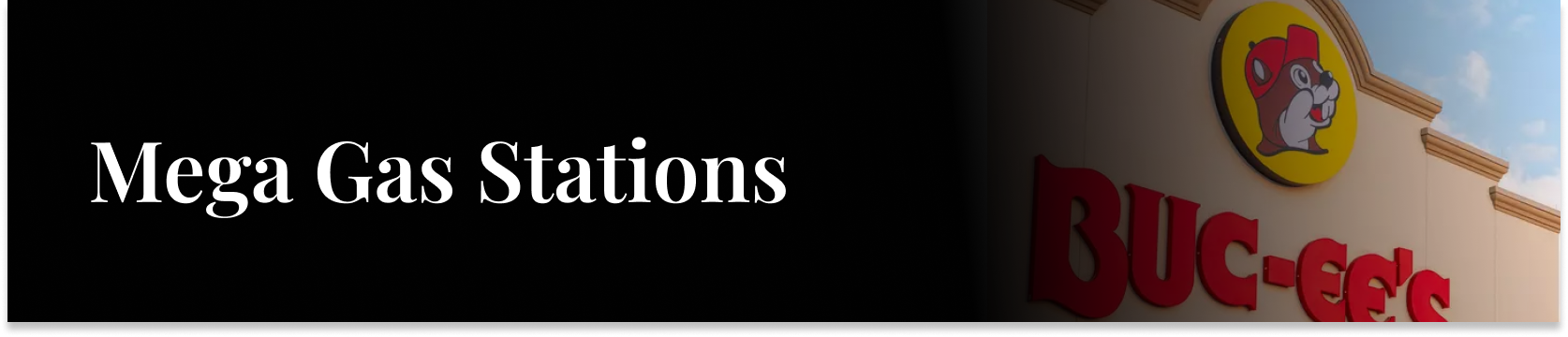

TL;DR: This July 4 weekend, millions pulled into what looks like a gas station and is actually one of the most profitable retail formats in America. Buc-ee's runs stores over 75,000 sq ft with 120 pumps; Dolly Parton just opened her own version. The secret: gas is a loss leader, earning 1-3% a gallon, often priced below cost, purely to pull cars off the highway. Two-thirds of revenue comes from inside, at 40% margins. Each store does $50-100M a year, roughly x10-18 the average c-store.

This past Fourth of July weekend, somewhere on an interstate, millions of Americans pulled into what looks like a gas station and is actually one of the most profitable retail formats in the country. Buc-ee’s, the Texas chain with the cartoon beaver, now runs stores over 75,000 square feet, half the size of a Walmart, with 120 pumps out front. Dolly Parton just opened her own version in Tennessee: 18 acres, a dog park, a theater, a bar, and 16 gas pumps. The gas is a loss leader. Fuel earns a razor-thin 1-3% a gallon, and Buc-ee’s often prices it below the competition, sometimes below what it paid, purely to get thousands of cars a day off the highway.

Two-thirds of Buc-ee’s revenue comes from brisket, Beaver Nuggets, $1,400 grills, and private-label merch at roughly 40% margins. Each store does an estimated $50-100M a year, somewhere between x10 and x18 the average American convenience store. The sign says gas station; the P&L says high-margin destination retailer that happens to own a very large fuel-price billboard. It’s the milk-at-the-back-of-the-grocery-store trick. Across the $837B convenience-store industry, in-store sales just hit a 22nd straight record year while fuel revenue actually fell, and prepared food has overtaken cigarettes as the biggest in-store category.

Buc-ee’s is quietly bolting on Tesla Superchargers, and a charge takes 20-30 minutes, which is 20-30 more minutes to sell someone brisket. The mega-store isn’t surviving the EV transition despite selling gas; it’s arguably the perfect business for it, a mall with a parking lot full of captive, bored, hungry people. The gas station that doesn’t need gas.

TL;DR: Jeff Bezos is raising $10B for Blue Origin at a $130B valuation, its first-ever outside round, riding the wake of SpaceX's record IPO. But $130B isn't Blue Origin's intrinsic worth, it's a number derived from SpaceX's, paid for a company whose flagship rocket exploded on the pad six weeks ago. The world can't afford only one Musk. When SpaceX switched off Starlink for Russian troops in February, one company moved a war. The bet is on optionality.

Jeff Bezos is raising $10B for his rocket company Blue Origin at a $130B valuation, its first-ever outside funding round after 25 years of Bezos quietly paying for it himself. The timing is not subtle: Musk’s SpaceX went public last month in the biggest IPO ever, at a $1.75 trillion valuation, and this looks like a bargain. $130B isn’t really Blue Origin’s intrinsic worth, it’s a number derived from SpaceX’s, and it’s being paid for a company whose flagship New Glenn rocket exploded on the launchpad six weeks ago.

The genuine case for Blue Origin isn’t that it beats SpaceX, it’s that the world can’t afford to have only one Musk. SpaceX is a NASA contractor with essentially no commercial rival, and back in 2024 a Pentagon panel explicitly warned against “dependence on a sole vendor.” Then in February we got the live demo: at Ukraine’s request, SpaceX simply switched off Starlink for Russian troops, and by one frontline account Russia lost half its offensive capacity overnight. One company, one man, one switch, moved a war.

Blue Origin is quietly pitching to new investors: TeraWave, its own satellite-comms network. A Starlink clone, funded specifically because the original Starlink has proven it answers to exactly one person. Call it the Lyft strategy (everyone wrote off the number-two pure-play for years, and it’s still here, minus the empire and the drama). You’re not paying $130B for the better rocket. You’re paying it so Musk isn’t the only phone number.

TL;DR: In an industry that competes on speed, the slowest player is quietly winning. Uniqlo releases 800 designs a year and plans production 12 months out; Zara does thousands and restocks every fortnight; Shein launches thousands a day. Yet Fast Retailing is now the world's #3 fashion retailer, shares up 74% in a year, and just posted a 46% jump in quarterly profit. The key isn't fashion, it's fabric science, and a 25-year partnership rivals can't copy. The biggest risk: its 77-year-old founder has no heir.

In an industry that competes on speed, the company quietly winning is the slowest one in the room. Uniqlo releases about 800 new designs a year and plans its production up to twelve months in advance. Zara pushes out thousands of designs a year and restocks every fortnight; Shein launches thousands of new items a day. And yet Fast Retailing, Uniqlo’s parent, is now the world’s third-biggest fashion retailer, about to pass H&M, with its share price up 74% in a year and having tripled in five. This week it reported a 46% jump in quarterly operating profit and raised its outlook for the third quarter running, an expected fifth straight year of record earnings.

The trick is that Uniqlo isn’t really in the fashion business, it’s in the basics business. It sells the same white T-shirt, black crewneck and puffer jacket year after year, tweaked but never overhauled. Because the range is small, it can sell a million units of one design where a fast-fashion rival sells under a hundred thousand, which hands it enormous scale advantages in fabric, sewing and dyeing. Founder Tadashi Yanai called it, back in 1991, “the McDonald’s of apparel”: a short menu of best-sellers, made cheap by volume, sold in neat folded stacks you browse like a bookshop.

Since 2000, Uniqlo has partnered with the Japanese chemicals giant Toray, which tested 10,000 prototypes to invent Heattech, a synthetic yarn that turns body moisture into heat. Uniqlo has since sold 1.5 billion Heattech garments. This is the whole strategic insight: a fashion trend can be copied in weeks, but a patented fabric built on a 25-year supplier relationship takes years and enormous losses to match. Uniqlo made a base layer into a product people search for, queue for, and re-buy every winter.

It’s the same move we keep seeing. Chanel bought its suppliers; Buc-ee’s owns the brand on its own snacks; Uniqlo consolidated from 300 factories to 50 and embedded itself so deeply with Toray that a rival can’t just show up and buy the same yarn. Control the input, own the margin, lock out the imitators. Uniqlo’s gross margin actually runs a touch below Zara’s, which looks like weakness until you realize it’s deliberate: it passes the savings to the customer, which is exactly why a brand born in Japan’s post-bubble deflation is perfectly built for a world that’s suddenly nervous, thrifty, and tired of disposable clothes.

None of which guarantees it works in America, the graveyard where countless foreign brands have died. Uniqlo itself flopped its first overseas push in Britain, closing most of its stores within three years, and stumbled in the US too before finding its feet.". The biggest risk is one man. Yanai is 77, has no named successor, and has ruled out his own sons. “It’s impossible to find another Mr Yanai,” says his own R&D chief. “Forget about it.” A company that built an unshakeable moat out of fabric science and supply-chain discipline still rests, at the very top, on a single 77-year-old who can sell you a billion T-shirts but can’t manufacture his own replacement.

TL;DR: This week a British startup sent an autonomous lab to orbit; another just raised the largest-ever seed round for making drugs in space. The reason is physics: without gravity, protein crystals grow far more perfectly. Cheap, repeatable launches turned microgravity into a rentable factory condition. Nobody's inventing drugs up there, they're reformulating existing IV blockbusters into at-home injections, which resets the patent clock. NASA and Merck already did it with a $29B cancer drug.

This week a British startup loaded an autonomous laboratory onto a SpaceX rocket and sent it to orbit, where it will study the proteins behind diseases like Alzheimer’s. It’s part of a small boom: another UK firm just raised the largest seed round ever for making drugs in space, and a handful of American companies are doing the same. Without gravity, molecules stop sinking and drifting, so protein crystals grow far more perfectly than they ever can on Earth. Cheap, repeatable, off-the-shelf launches have quietly turned microgravity into something you can rent by the mission, a factory condition like a cleanroom or a vacuum chamber, except the equipment is orbit itself.

They’re taking existing blockbusters, the ones that today require an IV drip in a hospital, and reformulating them in orbit into versions patients can inject at home. That does three things: moves the cost out of the hospital, expands the market, and, crucially, resets the patent clock, because a new formulation is new intellectual property and new years of exclusivity. This isn’t theoretical: NASA and Merck already used protein-crystal work on the space station to build an at-home version of Keytruda, a $29-billion-a-year cancer drug.

It’s the same thing that happened when cloud computing turned servers into a utility and a thousand software companies bloomed on top: once launch became a commodity you order off the shelf, the rocket stopped being the business and became the enabler of businesses. The value floats up the stack, from the launch to the payload. Largest-ever” seed round in this field is $13 million, the companies are years from real production, and the trillion-dollar space-economy forecast everyone cites has been the same tune for the last 8 years. Next it will be recreational drugs and space pirates.

TL;DR: A CBC investigation read StubHub's SEC filings and found the CEO, Eric Baker, co-owns a fund that sells millions in tickets on his own platform, and the company bankrolls other large-scale resellers. Roughly 70-80% of resale tickets are controlled by professional scalpers, not fans. It surfaced via the World Cup ticket fiasco, where StubHub advertised tickets a year before FIFA issued any. The tell was never hidden, it's in the prospectus. The IPO priced at half its target.

StubHub calls itself “a marketplace for fans to buy and sell tickets.” A CBC investigation this week read the SEC filings and found something else: the CEO, Eric Baker, isn’t just running the marketplace, he’s also part-owner of a fund called Andro Capital that sells millions of dollars of tickets on StubHub, and the company bankrolls other large-scale resellers through a financing affiliate. So the neutral venue is also one of the players, and roughly 70 to 80% of tickets on resale sites like it are controlled by professional scalpers, not the fan next to you who couldn’t make the game.

This surfaced because StubHub cancelled thousands of World Cup orders, stranding fans, including one in Vancouver who showed up to BC Place empty-handed. CBC found StubHub was advertising World Cup tickets a year before FIFA had issued a single one. That’s “speculative ticketing,” which is really just a naked short sold to a family: a scalper sells a ticket they don’t own, betting they can find one cheaper later, and when the bet fails, the loss lands on the fan at the turnstile while the platform keeps its fee. It’s banned in BC and Ontario; StubHub is spending money to kill a similar ban in California.

None of this is hidden: it’s all in the filings StubHub made when it went public last September, in the related-party notes where marketing claims go to quietly die. The IPO itself tells you plenty, priced at $8.6 billion, roughly half what the company wanted in 2024, shares down on day one, a $535 million loss on $9.2 billion of tickets sold, and a founder who owns single digits of the stock but 90% of the votes. Read the homepage and it’s a marketplace for fans. Read the prospectus and it’s a scalper with a controlling stake.

A YouTuber called Stevewilldoit walked into Mexico’s World Cup training camp before their last-32 game and handed every player a Rolex, about a million dollars in watches, $30,000 to $90,000 a wrist. It wasn’t generosity. He’d bet $2 million on Mexico to beat Ecuador, stood to clear a million in profit, and gifted that exact million in watches to the team he was betting on, which is either the world’s most confident hedge or the world’s most expensive good-luck charm. Mexico won that game 2-0. Then they gave all the watches back, because FIFA’s ethics code caps gifts at “symbolic or trivial value” and a $90,000 Rolex is neither, on pain of fines and a possible two-year ban. Days later Mexico lost to England and went home. The good-luck charm as it turned out, wasn’t.

“Gambling: The sure way of getting nothing for something.” — Wilson Mizner

Have a fantastic weekend. I welcome feedback and please forward this if you see fit.

Many thanks,

Sam.

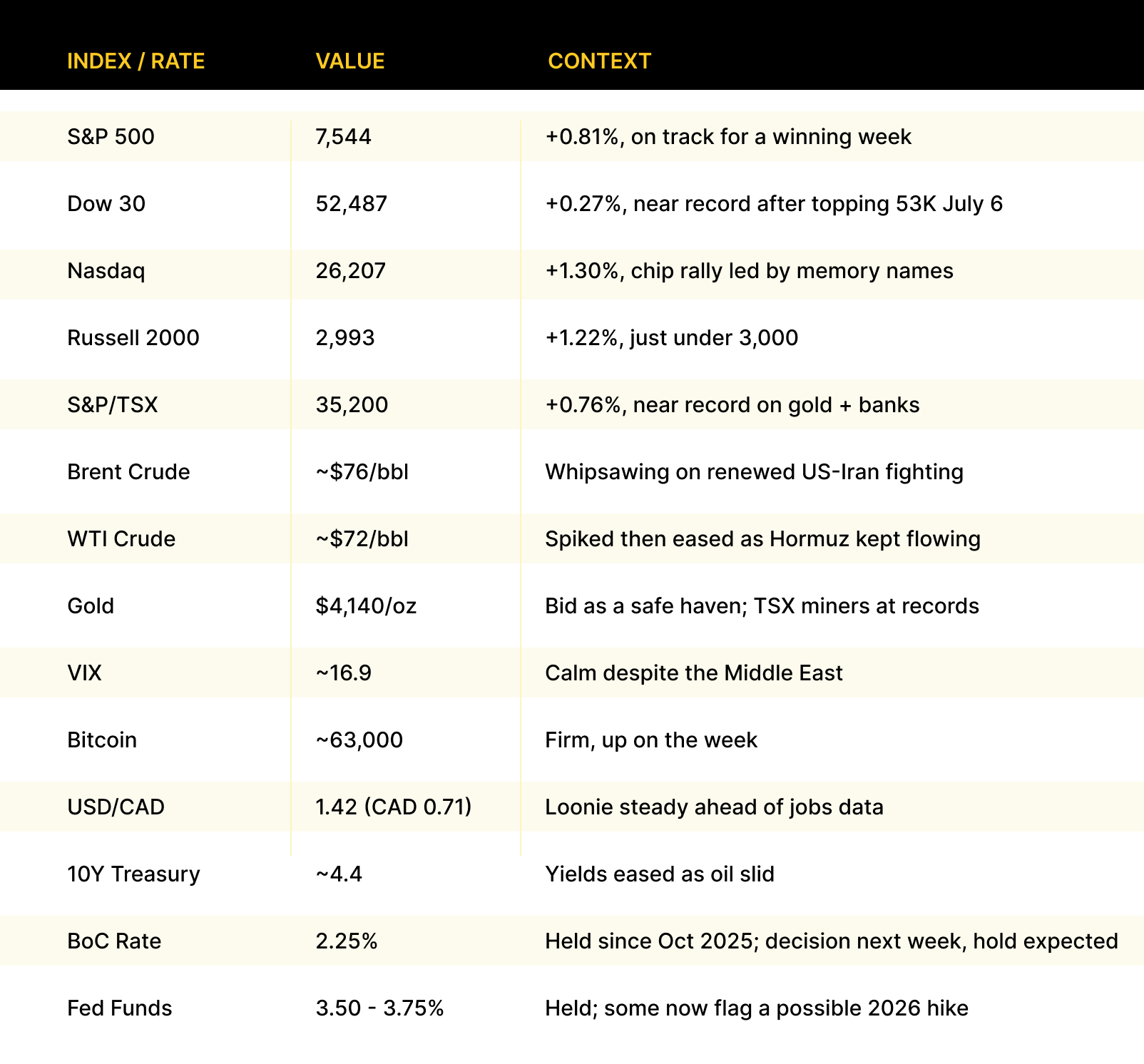

Market Snapshots

1 USD = 1.42 CAD = 0.86 EUR = 0.74 GBP at Thursday spot.

Sources

Daily Post Nigeria, Forbes, Celebrity Net Worth (opener); CNBC, NACS, MMCG, Payload/Management Consulted (Buc-ee’s); Semafor, CNBC, Bloomberg, TechCrunch, Forbes, BBC (Blue Origin / Starlink); FT (Harry Dempsey), Reuters, Nikkei, Fast Retailing IR, Goldman Sachs (Uniqlo); Semafor, BioIndustry, Payload, Morgan Stanley, MobiHealthNews (space pharma); CBC News (Dave Seglins et al.), StubHub SEC filings, CNBC, Forbes, TechCrunch (StubHub); The Athletic (Leon Imber), FIFA Code of Ethics (closer); CNBC, Yahoo Finance, Trading Economics, BNN Bloomberg, TMX, S&P Dow Jones Indices (market data).

Market data pulled Friday July 10, 2026 (July 9 closes). Live items this edition: the World Cup is in its late knockout rounds (final July 19); Blue Origin’s raise is reported, not yet closed; the CBC StubHub investigation published this week; the Uganda net-worth figures, Buc-ee’s/Dolly numbers, and Kaliningrad-style resale figures were current at press. The Iran ceasefire situation is moving. Currency at Thursday spot rates.