Clear Coca-Cola, Merck's $29B problem, QR codes vs Visa/MasterCard, A bank with wings, World Cup financial scorecard

39th Edition

Greetings folks and a warm welcome to the 39th Edition of Friday Finance,

Somewhere in New York you can now pay $500 for a woman in black to turn up at your funeral, weep quietly at the edge of the crowd, speak to nobody, and vanish before anyone can ask who she is. The company is called The Dark Secret, it takes Stripe, and it needs 48 hours’ notice. In its FAQ, when asked whether you can supply her with a backstory, the company says no: “The mystery is the product. A backstory is an answer. We sell only questions.” Asked about refunds, it says there are none, “you are, after all, not going to need the money.” So you prepay, in full, for a service you can never confirm was delivered, from a counterparty you cannot sue, on account of being dead. On that note, let’s get right to it.

TL;DR: In 1946, Coca-Cola made a colorless version of Coke so Soviet Marshal Zhukov could drink it without being seen enjoying American capitalism. Fifty cases, clear glass, white cap, red star. The flavor was unchanged; only the symbol changed. The payoff: Coke's trucks stopped getting held up crossing the Soviet occupation zone. That trick is now a multi-billion-dollar strategy: Russian crude gets refined in India and comes back to Europe as legal 'Indian' diesel, because once you refine it, the label stops saying Russia.

At the end of the war Eisenhower introduced Marshal Zhukov to Coca-Cola, and the man who took Berlin was hooked. The problem was that Coke had spent the war branding itself as America, and the Soviet Union’s greatest living war hero could not be photographed drinking a symbol of American capitalism. So Zhukov asked for a Coke that didn’t look like a Coke. The request went up through the American commander in Austria to President Truman, over to the chairman of Coca-Cola’s export arm, and a chemist stripped the caramel coloring out of the formula. Fifty cases were bottled in 1946 in clear glass, capped in white, with a red star stamped on top, so it could pass for vodka. The flavor was unchanged. Only the symbol changed. Coke’s trucks had to cross the Soviet occupation zone to reach Vienna, where everyone else’s freight sat for weeks waiting on Soviet paperwork. After Zhukov got his white Coke, Coca-Cola’s shipments were never stopped.

Under sanctions law, once crude oil is refined, it is no longer considered to come from the country the crude came from. The molecules do not change. The label does. So after 2022, Russian crude sailed to India, got refined in Gujarat, and came back to Europe as legal Indian diesel. India took 596 million barrels of Russian crude last year, about half of everything Russia shipped, and sent roughly 60 million barrels of refined product into the same EU that had banned Russian oil. In one quarter alone, about €1 billion of it. The single biggest node was a refinery in Gujarat that is 49% owned by Rosneft, the Russian state oil company.

Europe finally shut the loophole on 21 January this year, requiring importers to prove their crude wasn’t Russian, and flows from the implicated refineries fell 69% almost immediately. The loophole ran for four years. Refiners had insisted they kept separate production lines for Russian and non-Russian crude, which one analyst called probably untrue but useful for plausible deniability, and that is really what was being sold: not diesel, but a piece of paper that let Europe buy diesel. As for Coca-Cola, it ran the trick again. In 2022 the company left Russia, and its bottler relaunched effectively the same drink under a new name, Dobry Cola, in red cans, in a familiar font. It is now the best-selling cola in the country. In 1946 Coke changed its color to get into Russia. In 2022 it changed its name to stay.

TL;DR: The FDA just approved the first cholesterol pill of its kind, Merck's Lipfendra, an oral version of a drug that until now needed an injection. It works about as well as the shot, which barely sell ($4B combined) because people won't inject for a symptomless condition. In a pill, analysts think it could do $5B to $10’s of billions. The molecule barely changed; the delivery did. The real reason Merck needed it: Keytruda, 46% of revenue, loses patent protection starting 2028.

This week the FDA approved the first cholesterol pill of its kind, Merck’s Lipfendra, an oral version of a drug that until now required an injection. It lowers bad cholesterol by around 56 to 59%, which is roughly what the existing injectable versions already do. So the medical leap is modest. The commercial leap is enormous, and to see why, look at the injectables it’s copying: they cut cholesterol just as well, have proven they prevent heart attacks, and still only sell about $4 billion a year combined, because they come as a shot. It turns out that for a condition you cannot feel, people simply will not inject themselves (unless it’s for cosmetic reasons) Put the identical medicine in a daily pill, next to the statin 200 million people already take, and analysts think it could sell $5 billion to tens of billions.

The bigger reason Merck needed this is a number: $29 billion. That’s the roughly annual sales of Keytruda, its cancer blockbuster, which is about 46% of the whole company’s revenue and which starts losing patent protection in 2028. Merck is staring at the biggest patent cliff in the industry, and everything it’s doing right now is about what comes after Keytruda. A couple of weeks ago we wrote about Merck making a space-manufactured version of Keytruda to stretch its life; this cholesterol pill is the other half of the same problem, a fresh drug with a fresh patent clock in a large market, built to fill the hole.

Lipfendra is approved for lowering cholesterol, but hasn’t yet proven in a completed trial that it actually prevents heart attacks and deaths the way the injectables did; that study is still running. And it got fast-tracked through a new FDA “national priority” voucher, the kind of regulatory speed that’s quietly worth hundreds of millions in exclusivity. So Merck is selling convenience on a not-yet-fully-proven outcome, betting that the cholesterol number is enough. If they want real commercial traction, they should co-market it with a daily meal at McDonald’s and call it vertical integration.

TL;DR: The US just tariffed Brazil partly over Pix, a free government payment app that Visa and Mastercard called unfair competition. America is treating access to the dollar as a weapon, and the world is building payment systems it can't touch. The collateral damage is the card duopoly, which keeps 68 cents of operating profit per revenue dollar. Pix, India's UPI, Europe's Wero, and China's CIPS are all attacks on that toll. Fragmentation could cost 2.6% of global GDP by 2030.

This week the US formally moved to tariff Brazilian goods, and one of the cited reasons was a payments app. Pix, Brazil’s free, instant, central-bank-run payment system, now handles some $7 trillion a year and is used by 180 million Brazilians, and Visa and Mastercard complained to Washington that a free government utility amounts to unfair competition. Brazil’s response, from Lula on the left to a Bolsonaro on the right, was a unanimous shrug: Pix stays. America has started treating access to the dollar and its payment systems as a weapon, its own Treasury secretary calls it “economic statecraft,” and the rest of the world has quietly decided to build the exits.

Visa and Mastercard process about 85% of the world’s non-Chinese card payments and keep, around 68 cents of operating profit on every revenue dollar, a sovereign-level margin on a 60-year network that took two companies and almost no capital to build. Their crown jewel is cross-border payments, roughly a 3RD of revenue on a 1/10 of the volume, because international fees run about triple the domestic ones. That is exactly the money everyone else now wants to stop paying. When a duopoly earns like a sovereign, sovereigns notice.

There are 3 ways out, and countries are trying all of them. The first is to build your own: Brazil has Pix, India has UPI, and Europe is switching its national systems into a wallet called Wero and floating a digital euro by 2029. The second is to defect to the other superpower: China’s CIPS, its answer to the American-dominated SWIFT network, just hit record average daily flows of about $134 billion, up a fifth in a year, with a spike coming from Middle East oil being settled in yuan after the strikes on Iran. The third is to cut bilateral deals, plugging one country’s system straight into another’s; India is exporting UPI to nine countries with a sales pitch that is blunt about the point, that it will make you “sovereign.”

The thing that makes America’s financial plumbing powerful is the threat of being cut off from it. But every time that threat is used, or even implied, it hands every other country a reason to build plumbing that America cannot touch. Russia got cut off after 2022 and built its own card network and messaging system within months. Europe watched and started asking, out loud, what happens if Washington turns on us next.

None of which means Visa and Mastercard are going quietly. They’re building their own instant-payment rails, buying into local networks, Visa is partnering with China’s UnionPay, Mastercard is pouring money into data centers in France so it can call itself “a European network,” and above all selling the things a basic government bank-transfer can’t do, fraud detection, dispute resolution, the security layer. The likely future isn’t that the duopoly dies, it’s that it migrates, from owning the pipes to selling the safety features on everyone else’s pipes. It’s the same move Uniqlo and Chanel pull, retreat to the one layer that’s genuinely hard to copy. None of this is free: a study sponsored by SWIFT reckons the splintering could shave 2.6% off global GDP by 2030. Everyone gets more sovereign and slightly poorer at the same time. And the technology quietly dethroning the mighty American card networks, at the dead center of the biggest financial realignment in a generation, is the one piece of tech I personally cannot stand. Pix and UPI both run on QR codes. The QR code is winning a geopolitical war and I was thinking it was gone after COVID.

TL;DR: Americans are sitting on a record $38 billion pile of airline miles, and credit cards are now dictating routes, lounges, and gates. The reason: an airline makes 3-6 cents of profit flying you, and 50-70 cents on every dollar of miles it sells to a bank. Amex is on track to pay Delta $9 billion this year. The proof it's really a card company: during COVID, the loyalty programs were appraised at more than the airlines that own them.

Americans are sitting on a record $38 billion pile of airline miles, and the Wall Street Journal reports that credit cards are now the single sharpest advantage airlines have, dictating which routes they fly, where they build lounges, even which gates they fight for. An airline makes about 3 to 6 cents of profit flying you somewhere, and 50 to 70 cents on every dollar of miles it sells to a bank. American Express is on track to pay Delta around $9 billion this year, just for miles to hand out to cardholders. So the modern US airline is, financially, a credit-card company that happens to operate an airline, mostly as a way to sell you the card.

During the pandemic, with planes parked, the big three airlines borrowed against their frequent-flier programs to survive, and when the programs got appraised, they turned out to be worth more than the airlines that own them. American’s loyalty program was valued at roughly four times American Airlines itself, and more than Airbnb was worth at the time. Delta could raise more money pledging its miles program than pledging its entire fleet. The planes, it turned out, were the marketing department; the loyalty program was the business. Executives now say it plainly: JetBlue will fly a money-losing route if enough people on it carry its credit card.

All of this is funded by the swipe fee, the cut merchants pay every time a card is tapped, which gets baked into the price of everything, including for people paying cash who never earn a single mile. Your free business-class upgrade is quietly subsidized by the guy behind you buying groceries with a debit card. It’s a wealth transfer from cash-payers to points-optimizers, and the same lawmakers trying to cut those fees are the ones the airlines and banks are fighting hardest. An airline, it turns out, is a bank that owns some planes.

TL;DR: The final is Sunday, so here's the money scorecard. FIFA clears $8.9B from the tournament (part of a record $13B cycle), takes no risk, and even runs its own resale marketplace taking 15% from both sides. Its best trick: 'hydration breaks' that quietly created 7+ hours of new ad inventory worth $250M to Fox. Losers: fans ($32,970 final tickets), host cities (the $41B 'impact' mirage), and hotels (a 'non-event'). Betting is the other winner, $50B wagered.

The final is Sunday, Argentina against Spain, so here’s the money scorecard. The obvious winner is FIFA, which will clear around $8.9 billion from this tournament alone, part of a record $13 billion cycle, up from $5.3 billion just 8 years ago. FIFA is a Swiss non-profit that takes no risk and pays no dividends; it owns a fixed, irreplaceable cultural moment and sells it in pieces, to broadcasters, to sponsors, to fans. It even moved into ticket resale itself this year, taking a 15% cut from the buyer and the seller on tickets (some have been listed (but not sold) for over $2M). Two editions ago we called StubHub a marketplace secretly run by a scalper. FIFA just cut out the middleman and became one.

FIFA added mandatory water breaks for “player welfare,” which it insists earn it no additional revenue, and which happen to have created more than seven hours of brand-new advertising inventory in the one major sport that never had ad breaks. Fox, which paid $485 million for the US rights, could pull in $250 million from those breaks alone, at up to $750,000 for 30 seconds. It’s the White Coke move from earlier in this edition, applied to television: the same product, a commercial break, wearing a new label, hydration, and the new label is what gets it onto the pitch.

The losers are the people who had to show up. Fans paid up to $32,970 face value for a final ticket, and at one point $150 for a train ride to the stadium that normally costs $12.90; host cities got the usual mirage of “$41 billion in economic impact” that academics say never materializes, because the jobs are short-lived and low-paid and the stadiums already existed. “It creates jobs, but it does not create wealth,” as one put it. Hotels in Vancouver and New York, expecting a windfall, quietly reported a “non-event.” Meanwhile this is on track to be the biggest gambling event in history, around $50 billion wagered, and in the US states where betting is illegal, the action simply moved to prediction markets, which aren’t legally “gambling.” Call it a bet and it’s banned in Texas. Call it a market and it’s fine.

The man who runs Donald Trump’s teleprompter has operated it since 2016, which means that for years he has known exactly what the president is about to say before anyone else on earth does. This week we learned what he allegedly did with that edge. On the prediction market Kalshi, you can bet on whether specific words or phrases will come up in a speech, and Gabriel Perez, sources say, quietly wagered on more than a dozen of them and cleared over $100,000. Kalshi’s own surveillance caught it and flagged him to federal regulators, which is the part worth pausing on: the house turned in its own winner.

“The most valuable commodity I know of is information.”-Gordon Gekko, Wall Street

Have a fantastic weekend. I welcome feedback and please forward this if you see fit.

Many thanks,

Sam.

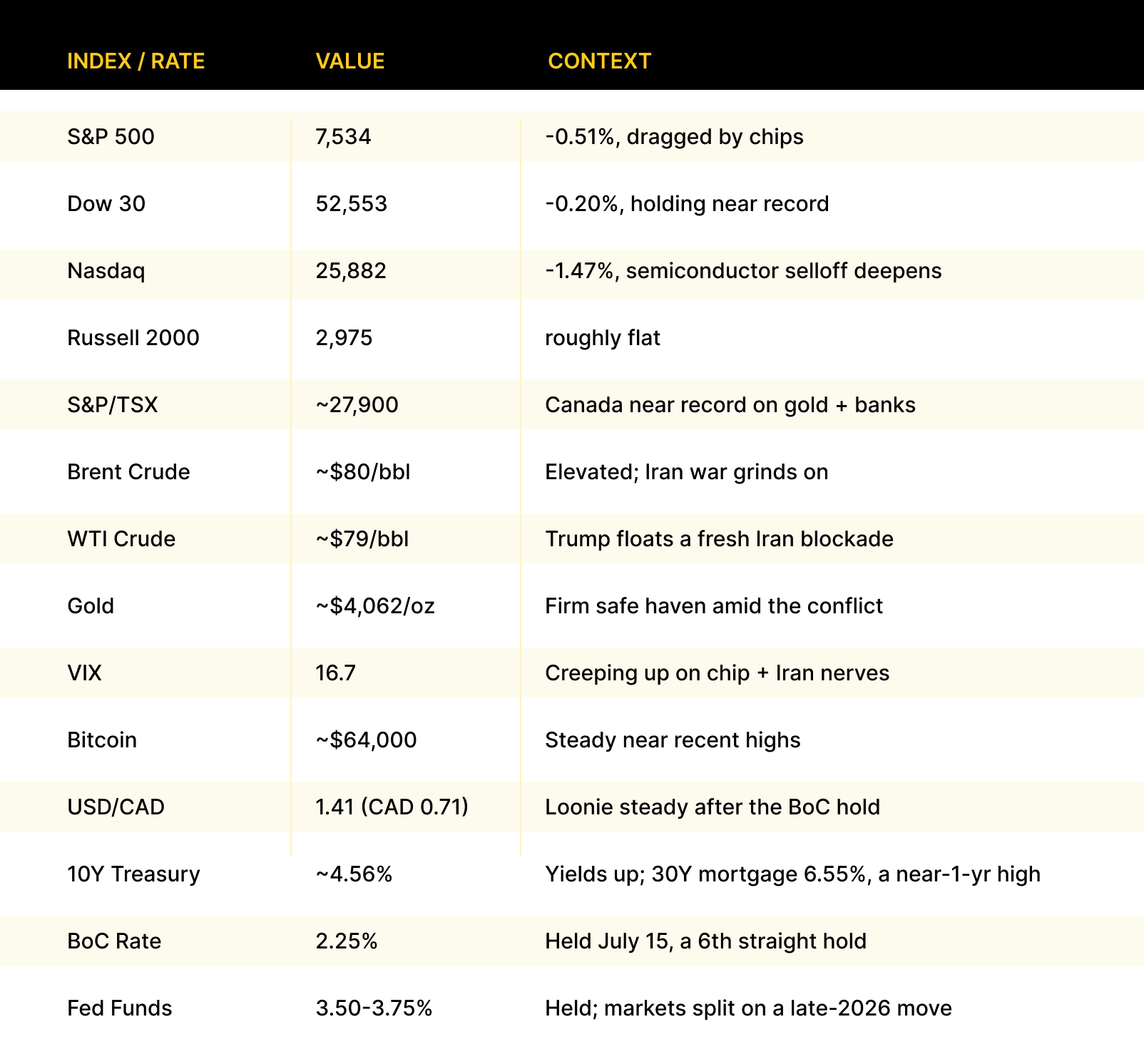

Market Snapshots

1 USD = 1.41 CAD = 0.86 EUR = 0.75 GBP at Thursday spot.

Sources

darksecret.nyc, Boing Boing (opener); Mark Pendergrast “For God, Country and Coca-Cola,” RFE/RL, Kyiv School of Economics, Vortexa, Reuters (White Coke); Merck, CNN, BioSpace, pharmaphorum (Merck); The Economist, USTR, PYMNTS, FXC Intelligence, McKinsey (payments); Wall Street Journal (Sider & Passy), McKinsey, On Point Loyalty, COVID securitization filings (airline points); BBC (Michael Race), Deutsche Bank Research, Macquarie, ESPN, Yahoo Sports (World Cup); ABC News, NPR, The New Republic (closer); CNBC, TheStreet, Bloomberg, BNN Bloomberg, Reuters, Trading Economics (market data).

Market data pulled Friday July 17, 2026 (July 16 closes). Live items this edition: the World Cup final is Sunday July 19 (Argentina vs Spain, no champion yet at press); the Brazil tariff and the Merck approval are days old; the Kalshi/teleprompter story is breaking and rests on anonymous sourcing; the Dark Secret, White Coke, and airline-points figures were current at press. The Iran conflict is moving. Currency at Thursday spot rates.