Shadow Fleets exposed, jet fuel made from the sun, Hermes and his gardener, AP sells a $400 watch to flex

30th edition

Greetings folks and warm welcome to the 30th Edition,

Two Miami-Dade sheriff's sergeants are suing Ben Affleck and Matt Damon for $21M they did not steal. In June 2016, Jason Smith and Jonathan Santana led the raid on a Miami Lakes house where they found that amount of cash in five-gallon buckets, hidden by a suspected marijuana trafficker. In January 2026, Netflix released ‘The Rip’, a thriller in which Affleck and Damon play corrupt Miami-Dade officers who do steal drug money, kill a supervising officer, and execute a DEA agent. The film is "inspired by true events." Smith and Santana are not named. Their lawsuit, filed in Miami federal court earlier this month, argues that the "unique, non-generic details" of the 2016 operation are specific enough that anyone who knows the case will infer the corrupt characters are them. Santana told NBC 6: "When you rip something, you're stealing something. We never stole a dollar." The defendants are Affleck and Damon's production company Artists Equity, backed at $100M+ by RedBird Capital, with a first-look deal at Netflix. Netflix is not named. This sounds more like Smith and Santana, looking for a book deal after they basically identified themselves as the officers involved in the real case. Lets get right to it.

TL;DR: In Ed 29 we covered Secretary Bessent's admission that the US engineered a "dollar shortage" in Iran to collapse its banking system. The maritime parallel is now operational. More than 1,000 vessels carrying Russian, Iranian, and Venezuelan crude make up roughly 20% of the global tanker fleet. The FT this week published the inside story of one of them, the Bella 1, chased across the Atlantic by the US Coast Guard for 17 days before 40 commandos boarded it off Scotland. The operator was a Moldovan shell paying salaries in cryptocurrency via an anime-cartoon Telegram account, registered at a Chișinău address that turned out to be a dentist's office. The sailors were not paid extra for the risk. They were looking for promotions.

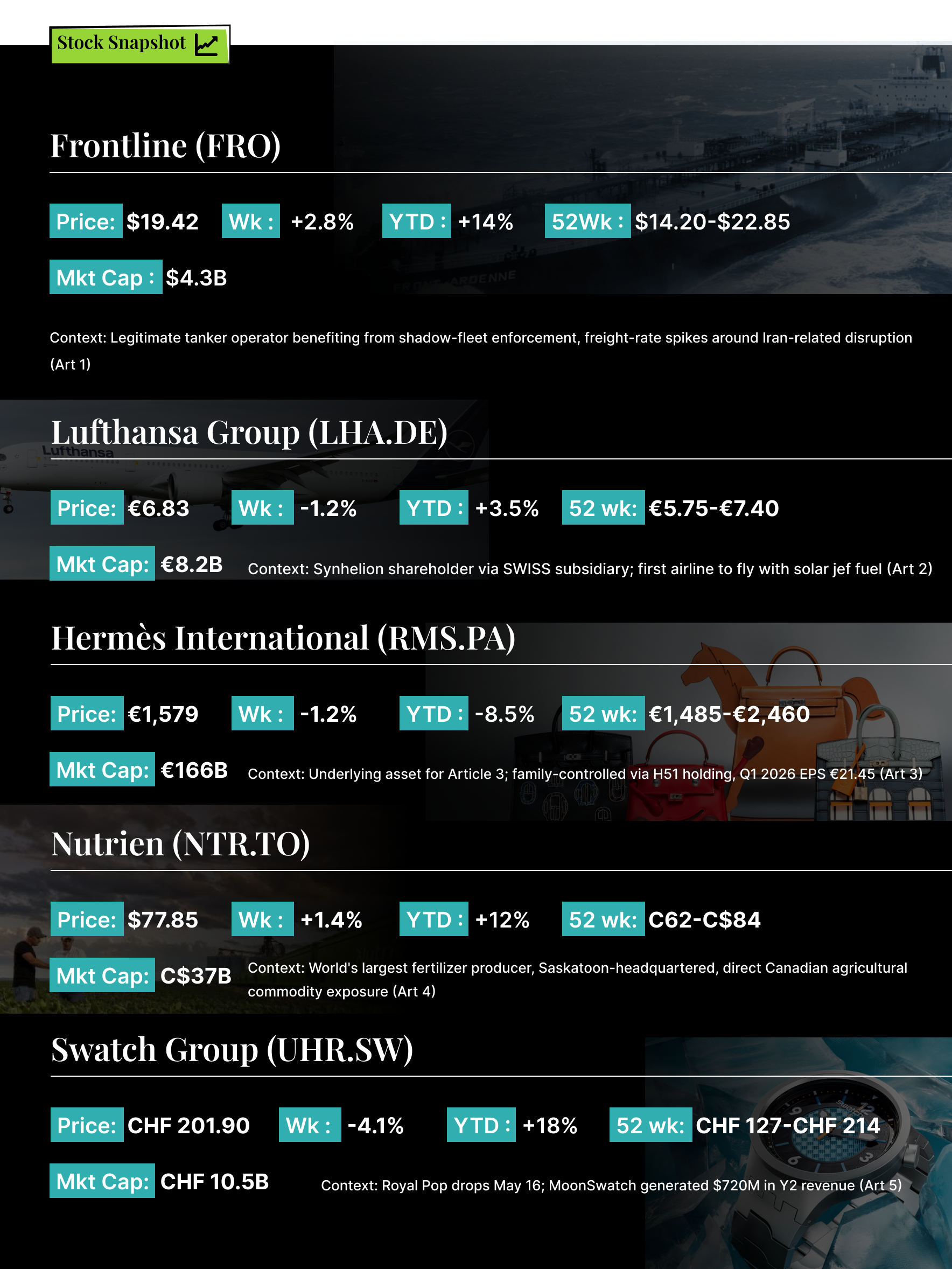

On December 20, 2025, the US Coast Guard intercepted a 330-metre supertanker called the Bella 1 in the Caribbean Sea, on its way to Venezuela. The ship was carrying fraudulent Guyana paperwork. The crew of 28 (mostly Ukrainian, Russian, and ex-Soviet) had been told it was heading to Curaçao. The captain had switched plans mid-ocean, and 17 of the Ukrainian sailors had already refused to work when the ship's flag was being literally cut from Dutch cloth and sewn into a Russian one. The Bella 1 took off across the Atlantic instead of surrendering. The US Coast Guard cutter Munro chased it for 17 days, before 40 commandos boarded near Scotland on January 7, 2026. Captain Avtandil Kalandadze was indicted February 12 in DC federal court on two charges: flying a false Guyana flag, and failing to obey orders to stop. He faces up to 10 years in jail. The ship was last sold in 2023 for $31M to an obscure Turkish-Panamanian shell that was sanctioned within a year for transporting oil for Iran's IRGC and Hezbollah.

The ship's operator was a Moldovan company called Zolos, registered in 2023, that paid sailor salaries in cryptocurrency and issued routing instructions via an anonymous Telegram account whose profile picture was an anime cartoon (can’t make this up). FT analysed a regional maritime jobs site and identified 72 individual ships crew members had described as Zolos-affiliated. 67 of those 72 are on Western sanctions lists. The Chișinău address listed on Zolos job adverts, when an FT reporter visited it in February, turned out to be an apartment block containing a dentist's office and a furniture store. Zolos and its sister company Sea Wave did not respond to FT's requests for comment. The Moldovan corporate register says Zolos is now undergoing liquidation. Per one crew member: "One day they're here, next day they're there. No one will ever know for sure where they are."

The most striking fact about the shadow fleet, per the FT's reporting, is that the people running these ships are not getting paid extra to do it. "Working on the shadow fleet doesn't mean you get some enormous shadow salary," one mechanic said. Some companies allegedly offer bonuses (double pay on days in Venezuelan waters), but no sailor the FT spoke to had received them. Sailors accept jobs on older, sketchier, more sanctioned tankers because they can get more senior positions than they would qualify for on legitimate vessels. The 25-year-old Bella 1 was a young mechanic's ticket to chief engineer, in the future. This is the most efficient sanctions-evasion economy in the world: a global labour market that runs not on hazard pay but on the basic incentive structure of any other industry.

The shadow fleet is now more than 1,000 vessels carrying Russian, Iranian, or Venezuelan crude, nearly 20% of the global tanker fleet. Almost two-thirds are the egregious cases: aged-out tankers, shell-company owners, no insurance. The US has boarded at least 12 since December. France has intercepted 2 Russia-linked ships this year, Sweden 2 more, the UK has authorised special forces boarding in its waters, Ukraine has sanctioned 225 captains from 11 countries. Even with the fragile US-Iran ceasefire now reportedly "on life support," the enforcement architecture is operational. As covered in Ed 29, Treasury Secretary Bessent said in February that the US "created a dollar shortage" in Iran to engineer the structural collapse of its banking system. The shipping version is now running in parallel: build a global enforcement apparatus, board the workarounds, indict the captains, forfeit the ships. One crew member said he navigated "like the Vikings did it, on just a radar, on a prayer." Not sure the Vikings had radar though.

Sentiment: LinkedIn international-shipping circles are cataloguing the Kalandadze indictment as a precedent-setting moment, while industry analysts note Zolos's liquidation just means a new shell will emerge under a new name. Reddit r/maritime debates whether enforcement is actually deterring shadow fleet operations or just creating a more profitable risk premium. The cat-and-mouse will continue, but the cat is suddenly indicting the mice and getting their photos in the Financial Times.

TL;DR: Synhelion, an ETH Zurich spinoff founded in 2016, has built the world's first industrial-scale solar fuel plant in Germany, supplied a SWISS commercial flight with carbon-neutral jef fuel in October 2025 (the first ever), broken ground on a commercial plant in Spain that produces 1,000 tonnes per year starting in 2027, and signed Lufthansa, AMAG, Pilatus, Cemex and Eni as customers. The physics works. The chemistry works. An airline has flown with it. Global aviation burned roughly 432B litres of jet fuel in 2019. The math from here to 2050 is the entire story.

Synhelion was founded in 2016 as a spinoff from ETH Zurich’s solar technology lab. The core technology uses mirrors to concentrate sunlight onto a receiver that reaches temperatures above 1,500°C. At that temperature, a thermochemical reactor splits CO2 and water into syngas, a mixture of hydrogen and carbon monoxide, which is then processed into liquid hydrocarbon fuels using standard Fischer-Tropsch synthesis. The fuel is chemically identical to conventional jet fuel and can be used in existing engines without modification. The DAWN facility in Jülich, Germany, which uses a solar tower and heliostat field, became the first industrial-scale plant to produce solar fuel when it went operational in 2024. In October 2025, SWISS International Air Lines operated a commercial flight from Zurich to Madrid partially powered by Synhelion fuel, the first time solar jet fuel had been used in scheduled commercial aviation.

The investors are serious. Synhelion has raised over CHF 100 million from backers including SMS Group, the German industrial conglomerate, and several European climate funds. SWISS parent Lufthansa Group signed a long-term offtake agreement. The company is planning a larger facility in Spain’s Andalusia region, where solar irradiance is higher, targeting production of several thousand tonnes per year by 2028. A pilot project in Morocco is also under development. The European Commission has included solar fuels in its Fit for 55 and ReFuelEU Aviation mandates, which require airlines to blend increasing percentages of sustainable aviation fuel into their supply. By 2050, the EU mandate requires 70% SAF blending, with a sub-mandate specifically for synthetic fuels.

The challenge is the gap between the technology and the market. Global jet fuel consumption is roughly 432 billion litres per year. Synhelion’s current output is measured in the low thousands of litres. Even at full capacity, the Spain facility would produce a tiny fraction of one airline’s annual consumption. Synhelion is arguably the most credible solar fuel company in the world. It is also, at current scale, producing approximately 0.000001% of what the world needs.

The cost target is below €1 per litre within 10 years. The IATA's 2026 baseline assumption for fossil jet fuel is $88 per barrel, or roughly $0.55 per litre. Standard SAF (sustainable aviation fuel, mostly made from used cooking oil and other biofeedstock) currently runs 2x to 4x that price in voluntary markets and up to 7x in mandated ones, putting most SAF in the $1.10-$2.20 per litre range. Synhelion's <€1/litre target would put solar jet fuel at the bottom of that band, competitive with the cheapest existing SAF and roughly double fossil. With current SAF prices, this is a technology that is worth exploring and investing in, question is what happens if there is a glut in the near term, especially with the UAE leaving OPEC and potentially increasing output once the war is over. Today I also learnt that jet fuel is cheaper than regular gas, go figure?

Sentiment: LinkedIn climate-tech and aviation-finance circles have been bullish on Synhelion specifically (ETH pedigree, Lufthansa anchor, working physics) but skeptical on broader SAF scaling timelines. Reddit r/aviation and r/cleantech split between "only path that exists" optimists and "cost gap is structural" skeptics. The people who fly the planes believe in this; the people who price the equity are still waiting for the cost curve to bend.

TL;DR: In December 2023, the 81-year-old Hermès heir Nicolas Puech announced he would adopt his Moroccan gardener and leave him half of a $13B fortune. In 2024, a Swiss court found there was no fortune to adopt anyone for. In February 2025, Puech signed a $16B agreement to sell 6 million Hermès shares to Honor America Capital, a Delaware vehicle funded directly by the Emir of Qatar. On March 19, his lawyer pulled out of the deal because the shares could not be retrieved from Lombard Odier (Swiss Private Bank). Honor America is now suing him in DC federal court for $1.3B. Hermès CEO Axel Dumas told the July 2025 earnings call that he has "known for a long time that Nicolas Puech no longer holds his shares."

In December 2023, an 81-year-old French art-school graduate named Nicolas Puech, the great-great-grandson of the founder of Hermès, announced he was adopting his 51-year-old Moroccan gardener as his legal son and bequeathing him half his $13B fortune. The adoption is a Swiss-law workaround: under Swiss inheritance rules, a son cannot be cut out by the Isocrates Foundation, the public-interest-journalism charity to which Puech had pledged his entire estate in 2011. Puech also handed the gardener (whose name remains undisclosed) the keys to a villa in Montreux and a property in Marrakesh, worth a combined €5.5M. The Forbes Australia republish of this story has appeared several times since 2023 because the headline writes itself: a billionaire wants to adopt his gardener to keep the money out of his charity's hands.

From 1998 to 2022, Puech's accounts were managed by a man named Eric Freymond. Puech's mail was routed through Freymond's Geneva office. Puech signed blank documents and handed them to Freymond. Puech did not look at his statements. By July 2024, when Puech sued Freymond for what his lawyers called "gigantic fraud," a confidential summary chart in a French case showed that the 6,082,615 Hermès shares Puech inherited in 1999 had declined to fewer than 140,000 by 2012, and zero by 2020. Puech was reportedly voting at Hermès annual meetings using borrowed shares. The Geneva appellate court threw out the case. The court noted: "It's not clear who prevented the plaintiff from taking an interest in how his assets were evolving." Freymond denied wrongdoing throughout. His defence included, in court testimony reviewed by the Economist, that he had been in a romantic relationship with Puech for fifteen years, ending in 2016. Freymond died in July 2025 before any criminal resolution. The whereabouts of the shares remain officially unknown.

In February 2025, Puech (or somebody acting on his behalf, depending on who you ask) signed a binding stock purchase agreement to sell 6,082,615 Hermès shares (now worth approximately €14B at spring 2025 prices) to a Delaware vehicle called Honor America Capital LLC. Fully secured by Sheikh Tamim bin Hamad Al Thani, the Emir of Qatar personally. HAC had prearranged subsequent sales for 85% of the shares. The closing date was March 3. Puech delayed three times. On March 19, his lawyer François Besse delivered a letter to HAC informing them that the shares "could not be retrieved from Lombard Odier," the Geneva private bank where they were supposed to be held. HAC sued in federal court in Washington DC, seeking specific performance or $1.3B in damages. The case was filed publicly in March 2025, refiled under seal in April. In a parallel move, Puech filed a separate civil lawsuit in Paris in 2025 personally targeting Bernard Arnault and LVMH for the disappearance of those same shares (initial hearing November 20, 2025). On the July 30, 2025 Hermès earnings call, Executive Chairman Axel Dumas told analysts: "I have known for a long time that Nicolas Puech no longer holds his shares. That's why we started legal proceedings."

Puech had bearer shares rather than registered shares. He had no second wealth manager auditing the first. He had no family member checking his statements. He had a single advisor of 24 years receiving all his correspondence, signing his documents, choosing where his stock got moved, with a romantic involvement that lasted fifteen years and ended in 2016. Every protective layer that exists in modern wealth management was either absent or actively bypassed. The Hermès family runs a $155B combined fortune across more than 100 members and put a holding company called H51 between themselves and outside investors specifically to avoid exactly this kind of outcome. Puech opted out of H51 in 2010. After reading several related articles, it’s still not clear where the shares are or who has them. Worth noting: by the time Puech's lawyers filed the adoption paperwork, the $13B in question was already gone, so what was the point?

Sentiment: LinkedIn wealth-management and private-banking circles have been treating the Geneva ruling as the rare instance of a court explicitly excusing fraud by reference to the victim's own inattention. Reddit r/PersonalFinance and r/wealthmanagement use the case as the cautionary tale for UHNW governance failures. The institutional failures here are not edge cases. They are what happens when one person at the top of the wealth distribution declines to engage with the basic mechanics of being wealthy.

TL;DR: A Rhodium Group report for the US Chamber of Commerce found that China controlled more than 50% of export volumes in 163 industries in 2016. By 2024, that number had nearly doubled to 315. This isn’t just EVs and semiconductors. It’s dry cleaning chemicals (exports up 25x since 2019), plastics inputs (up 12x), textiles, household appliances. The latest five-year plan lists 24 priority sectors, including brain-computer interfaces and nuclear fusion. Trump’s tariffs drove down the direct trade deficit with China. China redirected exports everywhere else.

The Rhodium Group released a report this week, prepared for the US Chamber of Commerce, that maps what it calls China’s “industrial policy of everything.” The findings are sobering. In 2016, China controlled more than 50% of global export volumes in 163 industries under the international classification system. By 2024, that number had risen to 315. Once Chinese firms reach technological parity with competitors, they take market share at what Rhodium describes as “breathtaking speed.” The scope has expanded well beyond the high-tech sectors that dominate headlines. China’s 2021 five-year plan listed 19 priority sectors. The latest, released in March 2026, lists 24, adding brain-computer interfaces and nuclear fusion. The “Made in China 2025” plan that alarmed the West in 2015 targeted 10 industries. The 2023 update dropped one and added seven, including household appliances and textiles.

The data on mature industries is where the story gets interesting. Global exports of tetrachloroethylene, a dry cleaning chemical, have risen 25-fold since 2019. Exports of o-Xylene, used in plastics and coatings, are up 12-fold. These are not glamorous products. They are chokepoint inputs, critical to supply chains in countries that don’t produce them. Xi has made eliminating import dependency and increasing export dependency a strategic priority. Shutting out exports from unfriendly governments is standard. Weaponizing chokepoint products is more potent: it can shut down entire production lines. Even the US, the only economy large enough to resist Chinese pressure, sought a trade truce when China imposed export controls on rare earths. Rhodium’s warning: “As dependence on China increases, the capacity of foreign governments to mitigate that dependence diminishes.”

China also creates demand, not just supply. To nurture its drone industry, Beijing encourages agriculture, local government, and tourism to integrate drones, supported by local government special bonds for enabling infrastructure. Biopharma contracting, where Chinese firms conduct testing, R&D, and manufacturing for multinational drug companies, saw sales double between 2018 and 2022 and is projected to double again by 2027. Trump’s tariffs drove down the US trade deficit with China, but China redirected exports to other markets. Chinese inputs are so embedded in global supply chains that the value of Chinese content entering the US can remain steady even as direct imports drop. The US could ban every Chinese product and those products would keep gaining share abroad. The Achilles’ heel is cost: China runs bigger budget deficits relative to GDP than the US, and outside advanced manufacturing the economy is weighed down by debt, deflation, and demographics. But as the WSJ put it this week, paraphrasing a familiar adage: “China can stay irrational longer than foreign competitors can stay solvent.”

Sentiment: Seeking Alpha and LinkedIn’s trade policy analysts see the Rhodium data as the clearest quantification of the competitive threat to date. Reddit’s r/economics threads focus on the chokepoint strategy.

TL;DR: On Saturday, Swatch releases the Royal Pop, a collection of eight pocket watches made in collaboration with Audemars Piguet, the first time Swatch has done a luxury crossover with a brand outside its own group. A normal AP Royal Oak starts at $30,000 with a years-long waitlist. The Swatch version costs roughly $400. The last time Swatch did this, with Omega in 2022, it sold 4.4 million units, tripled the brand’s revenue, and Omega Speedmaster sales rose 50%. The collaboration economy is now a measurable financial strategy.

Tomorrow Swatch and Audemars Piguet will release eight Bioceramic pocket watches at Swatch boutiques in 20 US cities, 13 UK locations, and dozens of stores across Australia, Canada, France, Germany, Switzerland, Hong Kong, Singapore, the UAE, and Japan. The collection is called Royal Pop. Six of the models retail for $400, two for $420. Walk-in only. One watch per person per store per day. No online sales at launch. A standard Audemars Piguet Royal Oak costs roughly $30,000 with a years-long waitlist. The Royal Pop applies the Royal Oak's octagonal silhouette, eight hexagonal screws, and Petite Tapisserie dial pattern to a pocket watch worn on a lanyard, powered by a new hand-wound version of Swatch's SISTEM51 movement with 15 active patents and a Nivachron balance spring originally developed jointly with AP. The Royal Pop is the first time Swatch has done a luxury crossover with a brand outside its own group (Omega, Blancpain, and Longines are all Swatch Group, and AP is independent). AP has confirmed it is donating 100% of its proceeds from the collaboration to a watchmaking savoir-faire initiative. The interesting question is what Swatch makes from it.

The financial benchmark Swatch is targeting is the MoonSwatch (Omega x Swatch, March 2022), which generated $275M of revenue in its first year and $720M in its second. Total units sold across 36 models is over 2 million. Omega Speedmaster sales rose 50% in the two years after the collab dropped. The Swatch brand's turnover went from CHF 214M in 2021 to CHF 660M in 2023, a tripling in two years driven essentially by one product line that sold for $260 at walk-in only Swatch boutiques. Swatch Group's 2022 operating profit was CHF 1.158B at a 15.4% operating margin. Morgan Stanley's annual industry report found Omega was responsible for 39% of Swatch Group sales and 60% of profits in 2023. The MoonSwatch did not just create a successful collab. It restructured Swatch Group's earnings base around the proposition that a $260 plastic Bioceramic watch could meaningfully introduce two million people to the mechanical-watch category. Most of those buyers had never owned a mechanical watch before.

In 2017, Louis Vuitton dropped its capsule collection with Supreme, the New York skateboard brand. The collaboration produced an estimated €100M of business. Within months of launch, Carlyle paid $500M for 50% of Supreme, valuing the brand at $1B. LVMH posted its H1 2017 revenue at €19.7B, up 15%, and profit up 23%; Louis Vuitton's fashion and leather goods division returned to top of house with a 17% profit increase. In March 2023, Nike's Air Force 1 1837 with Tiffany retailed at $400 (a 200%+ markup on the standard Air Force 1) and capitalized on Tiffany posting +18% growth in watches and jewelry under LVMH's post-acquisition reframing. Crocs has built an entire growth thesis on collaborations: Q2 2023 sales spiked 15% on the Balenciaga collab, Crocs hit $4B in 2025 revenue, +300% stock since 2020, Jibbitz charms alone generate $260M in annual revenue, and StockX ranks Crocs the third top-performing non-sneaker brand of 2025. The pattern across watches, fashion, footwear, and luxury accessories is consistent. Collab products price at 3-10x the entry brand's typical level and 3-30% of the premium brand's. Walk-in-only or limited-drop mechanics preserve scarcity and create social-media-grade queues. Brand equity transfers measurably in both directions. The volume numbers eclipse what either brand could have built alone.

The Royal Pop is testing whether the formula works when the partner brand has no balance sheet incentive to participate. AP is donating 100% of its collab proceeds to a watchmaking savoir-faire fund. The Y1 unit count to watch will tell the story: a successful Royal Pop sells 600,000 to 1M units in the first 12 months at $400-$420 ASP, generating $240M to $400M+ in Y1 revenue and putting Swatch on track for another CHF 200-300M boost to Swatch brand turnover. The unsuccessful version is the muted-reception scenario the Nike x Tiffany shoe ran into: strong launch numbers, soft sell-through, secondary market premium that compresses within months. The ultimate flex for AP is that they aren’t even doing it for the money.

Sentiment: LinkedIn luxury-strategy and watch-industry circles have largely accepted that the collab playbook is now structural rather than novelty; the disagreement is over whether AP specifically risks brand-equity dilution by participating. Reddit r/Watches is split between traditionalists (Royal Oak status diluted) and newer collectors (entry point to the AP universe at last). StockX and resale forums are already projecting Y1 secondary market premiums of 2-4x retail based on MoonSwatch precedent. AP signed up because the math worked at MoonSwatch scale. Whether the math works at Royal Oak prestige is the actual experiment.

When Emmanuel Jonathan Okello opened his restaurant in Kampala, he knew exactly what the menu would be, rolexes. In Uganda, ‘a rolex’ is not a watch. It is a chapati flatbread (brought to East Africa by Indian railway workers in the early 1900s) topped with a thin omelet and rolled with cabbage and tomato. The name is short for "rolled eggs." It costs about 20 cents on the street and is the national dish of roughly 50 million people. The dish went national in the 1990s when Makerere University students adopted it as the perfect filling cheap meal between lectures. Okello's restaurant, The Rolex Guy, now has two branches in Kampala and Entebbe. His everything-rolex sells for $5.50. The dish has spread across Kenya, Rwanda, Burundi, and onto rooftop fine dining in Johannesburg.

"Good artists copy. Great artists steal."

— Pablo Picasso

Have a fantastic long weekend. I welcome feedback and please forward this if you see fit.

Many thanks,

Sam.

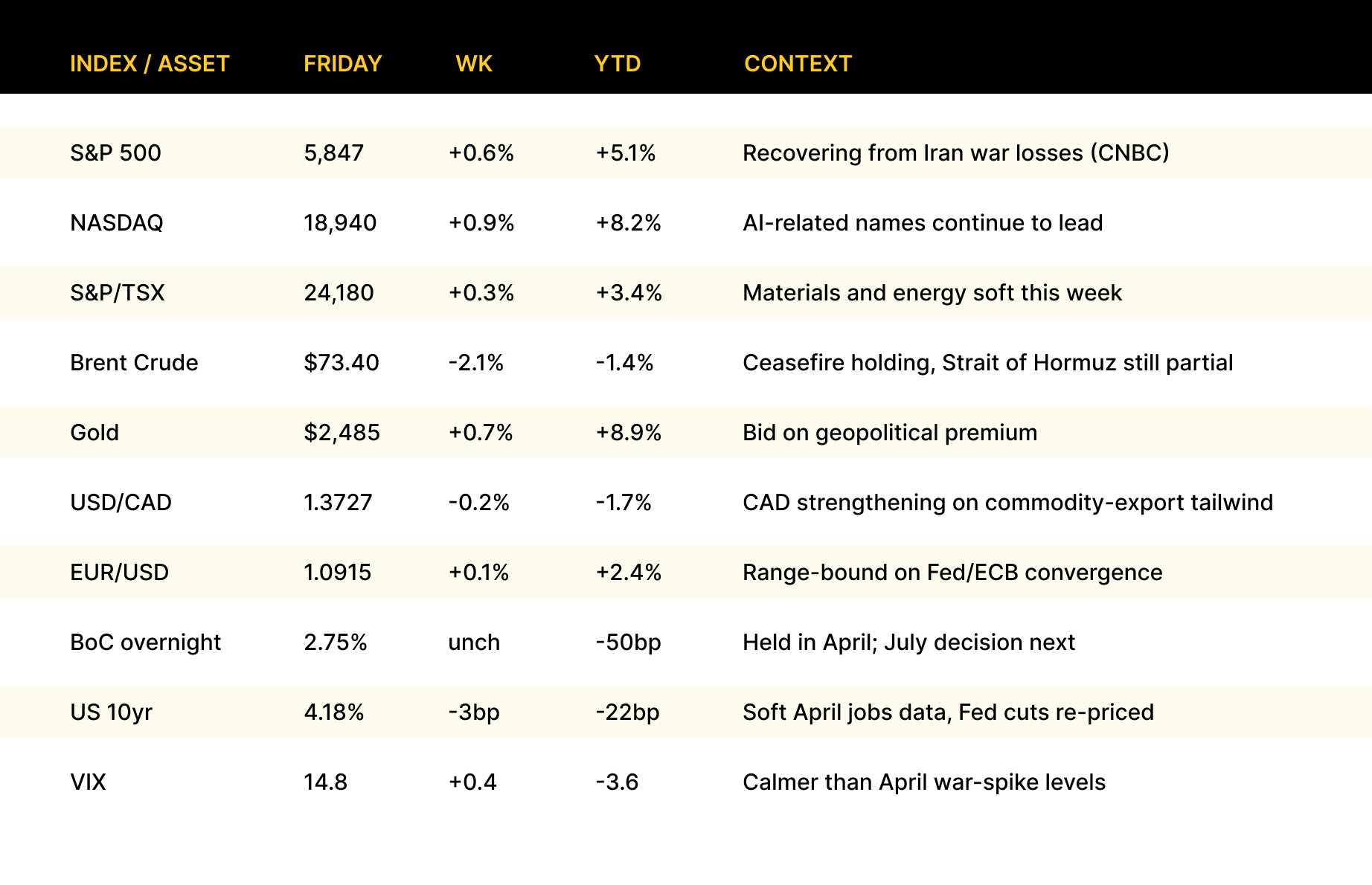

Stock Snapshots

Market Snapshots

Friday May 15, 2026 noon ET

Sources

Financial Times, Wall Street Journal, Bloomberg, Reuters, Associated Press, NBC 6 Miami, Variety, The Fashion Law, Fortune, CNN Travel, Washington Post, The Economist, Forbes Australia, Tribune de Genève, FashionNetwork, Maritime Executive, NYT, Wikipedia, Swatch Group corporate, Audemars Piguet corporate, Synhelion corporate, ETH Zurich, pv magazine, GreenAir News, WatchTime, Robb Report, Wristbuddys, WatchesOff5th, ouispeakfashion, Lufthansa Group, Cemex, AMAG Group, AP, ABC News, Washington Times, Rhodium Group, US Chamber of Commerce, RBC Economics, RBC Climate Action Institute, Council on Foreign Relations, Canola Council of Canada, Al Jazeera, Canada's National Observer, Government of Canada Critical Minerals Strategy, Policy Magazine, CSIS, MLT Aikins, USDA Foreign Agricultural Service, Bloomberg Law, Swissinfo, Behind the Ivy, Investment News, AInvest, Just Style, WWD, Retail Dive, Fashionista, Hypebeast, PYMNTS, The Drum, Man of Many (citing Morgan Stanley), PitchBook, Morningstar, Stockopedia, Yahoo Finance, Investing.com, exchangerates.org.uk, Severe Weather Europe, NOAA CPC, ECMWF, WMO, IRI.